Biosimilar Reimbursement: What You Need to Know About Cost, Coverage, and Access

When you hear biosimilar reimbursement, the process by which health insurers pay for biosimilar drugs that mimic complex biologic medications. Also known as biologic drug coverage, it's not the same as covering a regular generic pill—these are intricate, living-based treatments that cost less but require special rules to approve. Biosimilars aren’t copies like aspirin alternatives. They’re made from living cells, so even tiny changes in production can affect how they work. That’s why insurance companies treat them differently—and why understanding reimbursement rules can save you thousands.

Many patients are switched to biosimilars without knowing why. Insurers push them because they cost 15% to 35% less than the original biologic drugs like Humira or Enbrel. But not all doctors are comfortable with the switch. Some worry about how well biosimilars perform long-term, especially for autoimmune diseases like rheumatoid arthritis or Crohn’s. A biosimilar, a highly similar version of a brand-name biologic drug approved after the original patent expires must meet strict FDA standards, but real-world use still raises questions. Meanwhile, drug coverage, the extent to which insurance plans pay for prescription medications varies wildly by state, plan type, and even the pharmacy you use. Some plans require prior authorization. Others only cover biosimilars if you’ve tried the brand first. And in rare cases, patients must prove they can’t tolerate the original drug to get it covered.

It’s not just about money. insurance for biosimilars, the policies and procedures that determine whether a health plan will pay for a biosimilar medication often include step therapy rules that delay access. Patients who’ve been stable on Humira for years might be forced to switch, even if they’re doing fine. That’s where generic biologics, an informal term sometimes used to describe biosimilars, though technically inaccurate since biosimilars are not generics get misunderstood. They’re not generics. They’re not cheaper versions of the same chemical. They’re complex, highly similar, but not identical—and that’s why some doctors hesitate. But here’s the thing: studies show most patients do just as well on biosimilars. The real barrier isn’t science—it’s policy, paperwork, and lack of provider education.

What you’ll find in the posts below isn’t just theory. It’s real-world guidance: how to talk to your doctor about staying on your current biologic, why some insurers still resist biosimilars, and how to fight denials. You’ll see how cultural beliefs affect trust in these drugs, how pharmacies handle substitution, and what to do when your plan refuses to cover the medication you need. This isn’t about choosing between brand and generic. It’s about understanding a new layer of healthcare economics—and getting the treatment you deserve without unnecessary hurdles.

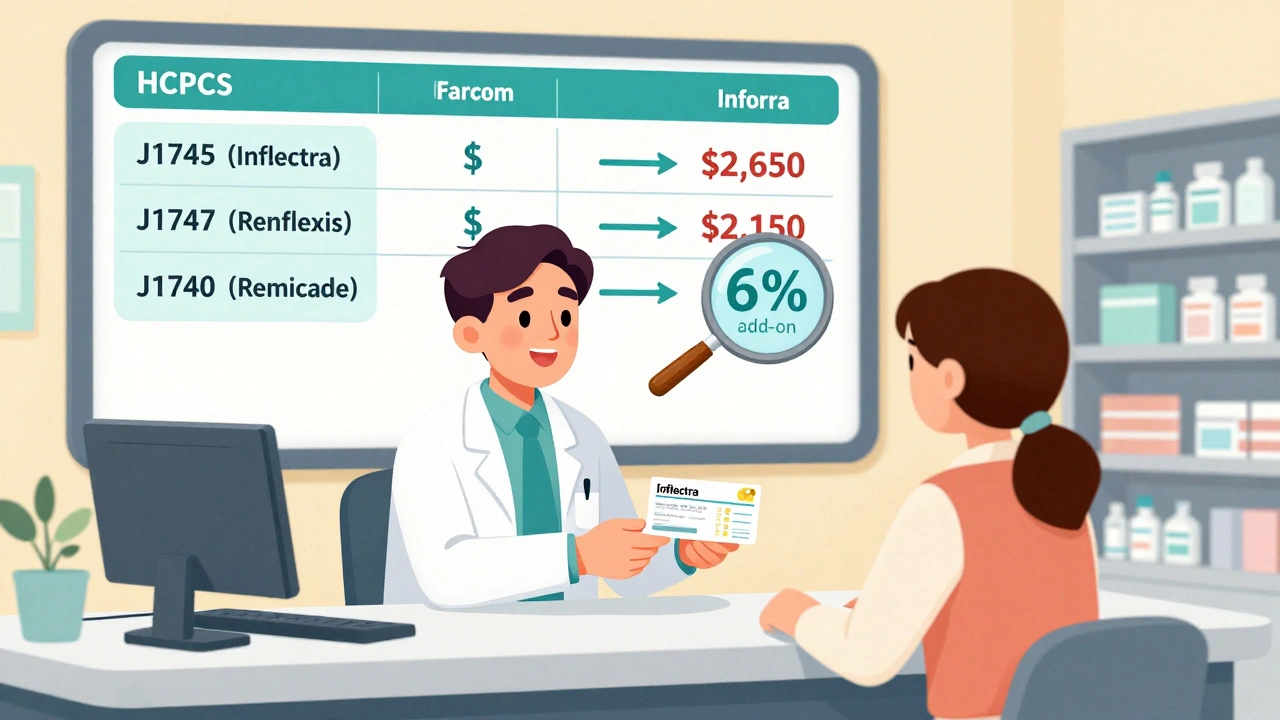

Reimbursement and Coding for Biosimilars: How Billing Works Under Medicare Part B

Learn how biosimilars are billed under Medicare Part B, including HCPCS coding, reimbursement calculations, the JZ modifier, and why adoption remains low despite cost savings. Understand the system providers use and how it affects patient access.

Read more